The latest CIRAD data reveals a record-breaking European supply glut — and a strategic argument for why Kenya’s avocado future belongs in China.

Week 21 of 2026 will be remembered by European avocado traders for a long time. According to the CIRAD Weekly Avocado Report, a total of 6.9 million 4-kg boxes arrived on the European market in a single week — the highest weekly volume ever recorded. Prices for the benchmark Hass grade 18 fell to €8.81 per box, down 25% against the 2023–24 average.

For East African suppliers — including Kenya — the numbers are sobering. Kenya currently holds just a 2% share of the European market, and volumes remain well below historical averages, down 55% year-on-year for the season to date. Small-scale suppliers from the region are being singled out in trade reports as suffering from a “reputation deficit,” squeezed out by buyers who are now fiercely loyal to Peruvian and South African brands.

Peru has shipped 35.6 million boxes into Europe this season alone, up 25% on last year and 42% on 2023/24. Their coastal production transition has improved quality and consistency. The result: European buyers have consolidated around Peruvian fruit for retail programs, and premium shelf space is effectively closed to smaller origins.

The contrarian read: this is good news for Kenya’s China pivot

There is a different way to read this data entirely — and it points directly east. The same report shows Peru directing 16% of its exports to Asian markets, with the US market now absorbing further diverted volumes following a sharp price spike of $7–10 per box in Week 21. Peru is stretched across three major markets simultaneously. China remains significantly undersupplied relative to its growth trajectory.

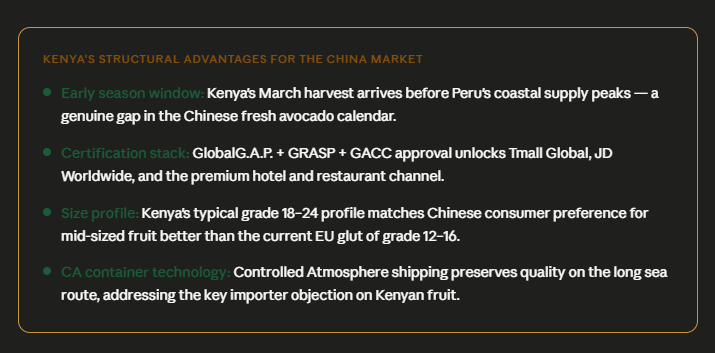

Kenya’s competitive window is not in slugging it out for a 2% European market share against a supplier shipping 4.9 million boxes a week. It is in offering Chinese buyers something Peru cannot easily replicate at scale: early-season certified fruit in March and April, before the Peruvian coastal surge even begins, backed by GlobalG.A.P., GRASP, and GACC credentials that unlock e-commerce and premium retail channels.

Early season window: Kenya’s March harvest arrives before Peru’s coastal supply peaks — a genuine gap in the Chinese fresh avocado calendar.

Certification stack: GlobalG.A.P. + GRASP + GACC approval unlocks Tmall Global, JD Worldwide, and the premium hotel/restaurant channel.

Size profile: Kenya’s typical grade 18–24 profile matches Chinese consumer preference for mid-sized fruit better than the current EU glut of grade 12–16.

CA container technology: Controlled Atmosphere shipping preserves quality on the long sea route, addressing the key importer objection on Kenyan fruit.

What the price collapse reveals about market structure

The CIRAD data makes one thing clear: the European avocado market has structurally changed. When a single origin — Peru — commands 70% market share and ships record volumes, price discovery breaks down for everyone else. South Africa, Brazil, and East Africa are all being forced into aggressive discounting simply to maintain sales momentum. This is not a cyclical dip. It reflects a structural consolidation that smaller origins cannot price-compete their way out of.

The China market, by contrast, is still in a growth and diversification phase. Chinese importers are actively seeking reliable, certified origins as a hedge against over-dependence on Peru and Chile. The conversation Xcado is having with buyers — from COFCO/Fujian Tea’s trading network to Tmall Global — is one of partnership and channel-building, not commodity pricing.

Our position

At Xcado, we read the CIRAD report each week not as a verdict on our business, but as a navigation tool. Week 21’s data reinforces every strategic choice we have made: building GACC registration, developing Sea CIF Shanghai pricing for both 4kg retail and 10kg wholesale formats, and targeting the March–April window when Kenya’s supply is at its peak and European pressure is at its lowest.

The European market will recover. Peruvian supply will moderate. But the more durable opportunity — the one worth building infrastructure and relationships for — is the Chinese market, where Kenya’s fruit arrives with a story, a season, and a certification stack that no amount of Peruvian volume can replicate.